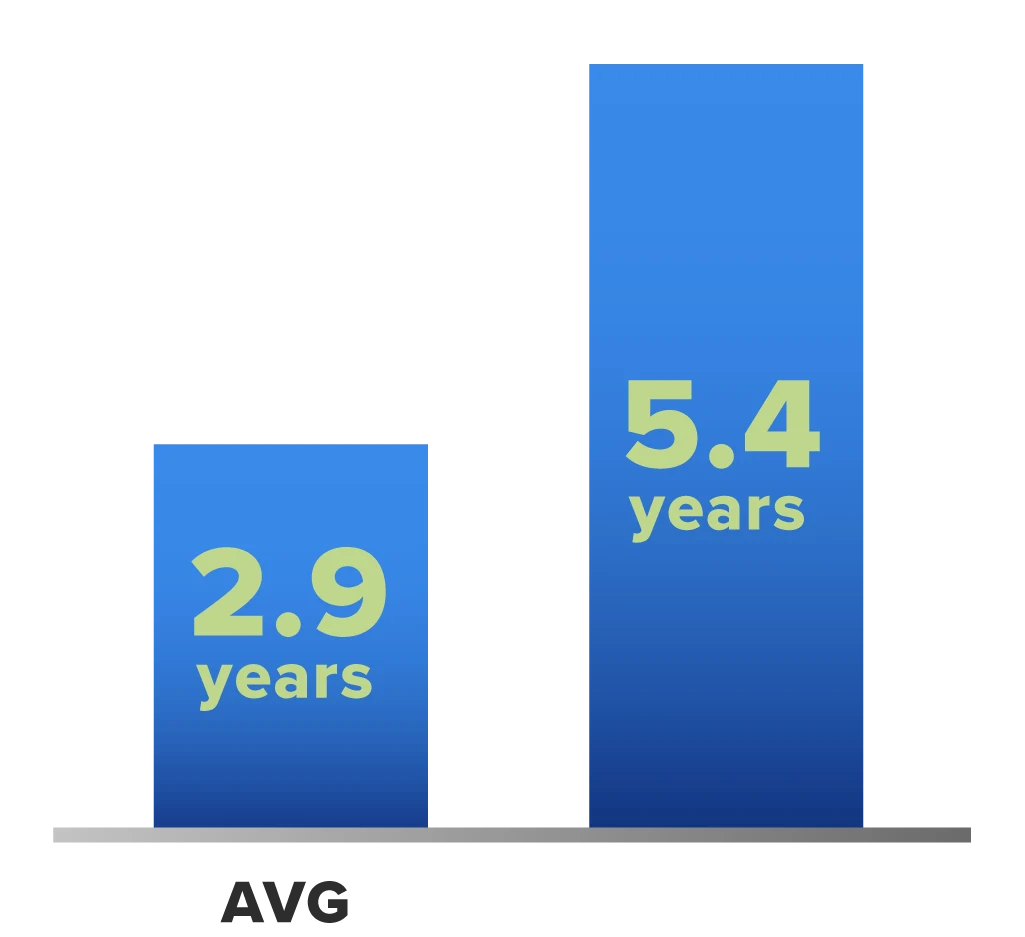

Increase Retention

Companies with robust internal mobility retain employees nearly

2x longer (5.4 yrs).

Keep your best employees longer and fill skills gaps from within while attracting top talent.

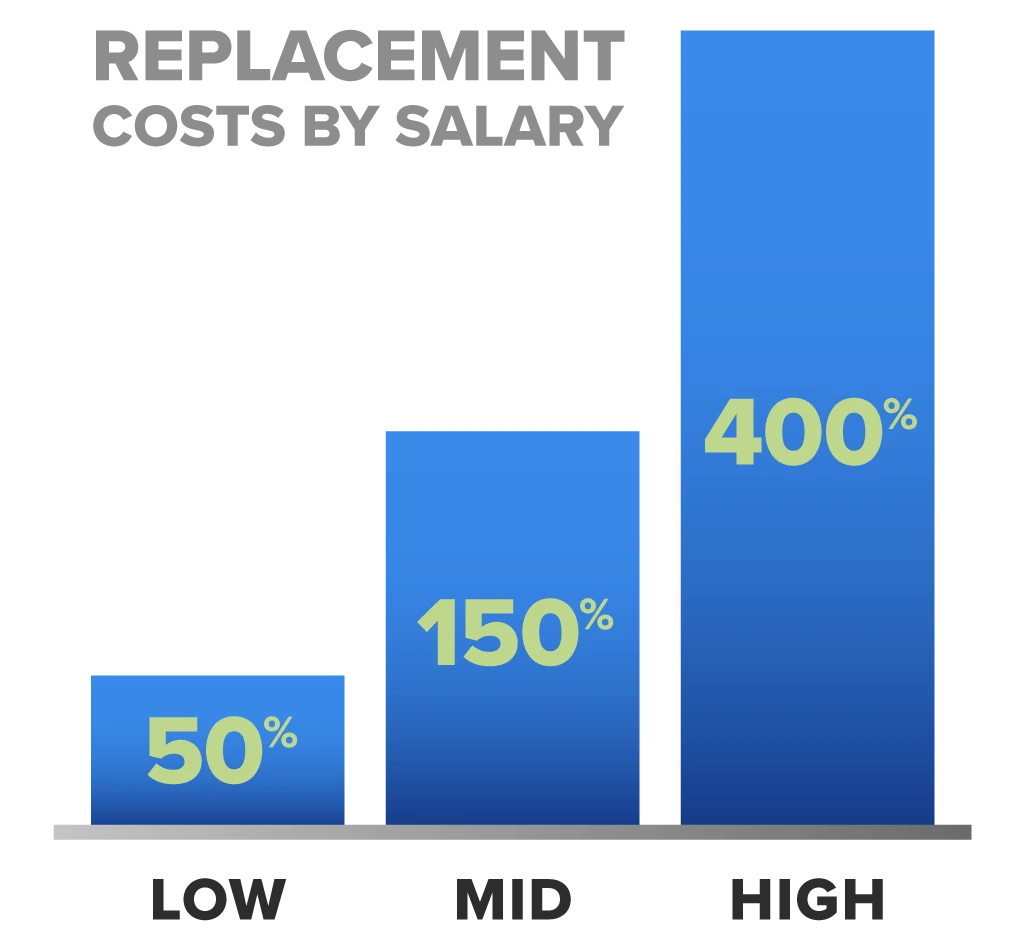

Increase ROI

The cost of replacing a candidate is 0.5-4x their annual salary.

Increase productivity, earn client trust, and get your employees to licensure and certification faster.

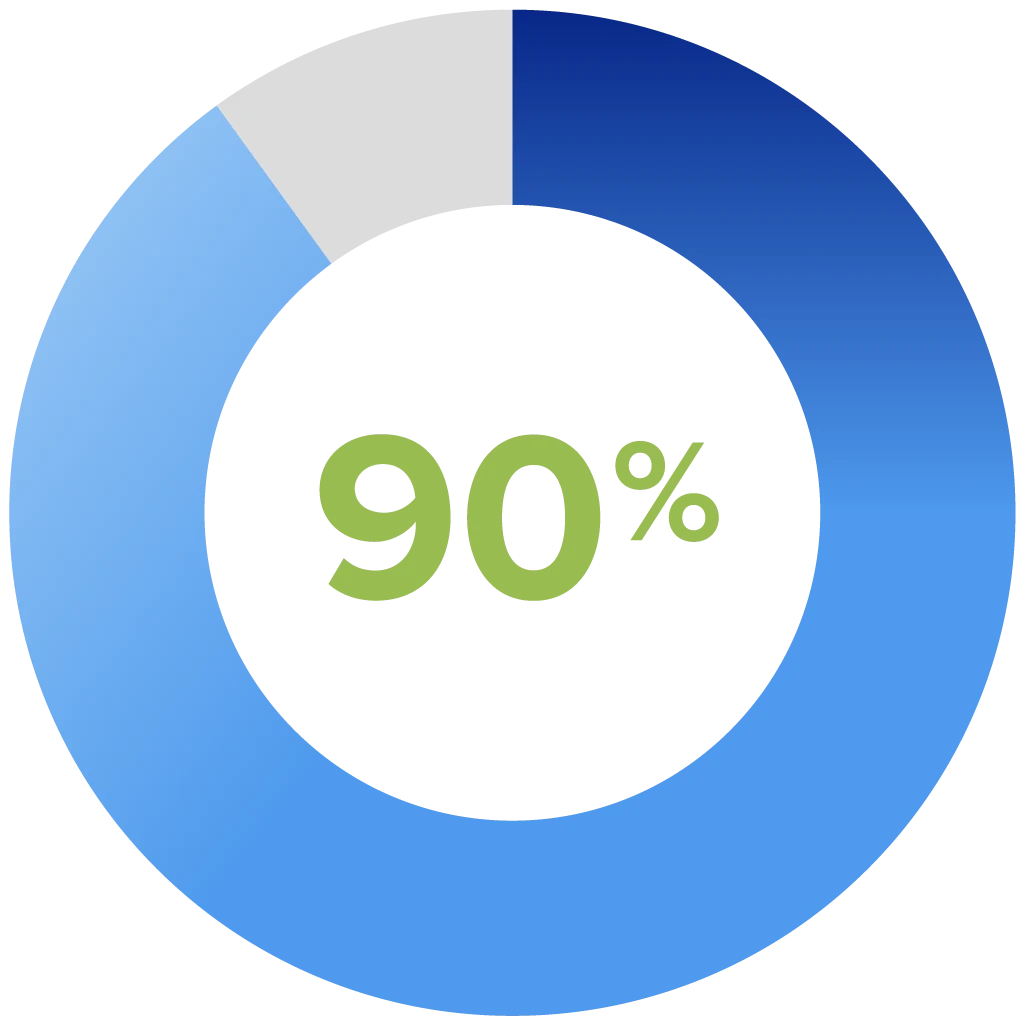

Increase Engagement

Objectives will be met

90% more often by

increasing team skills.

Build a culture of continuous learning that fosters intellectual curiosity and adaptive thinking.

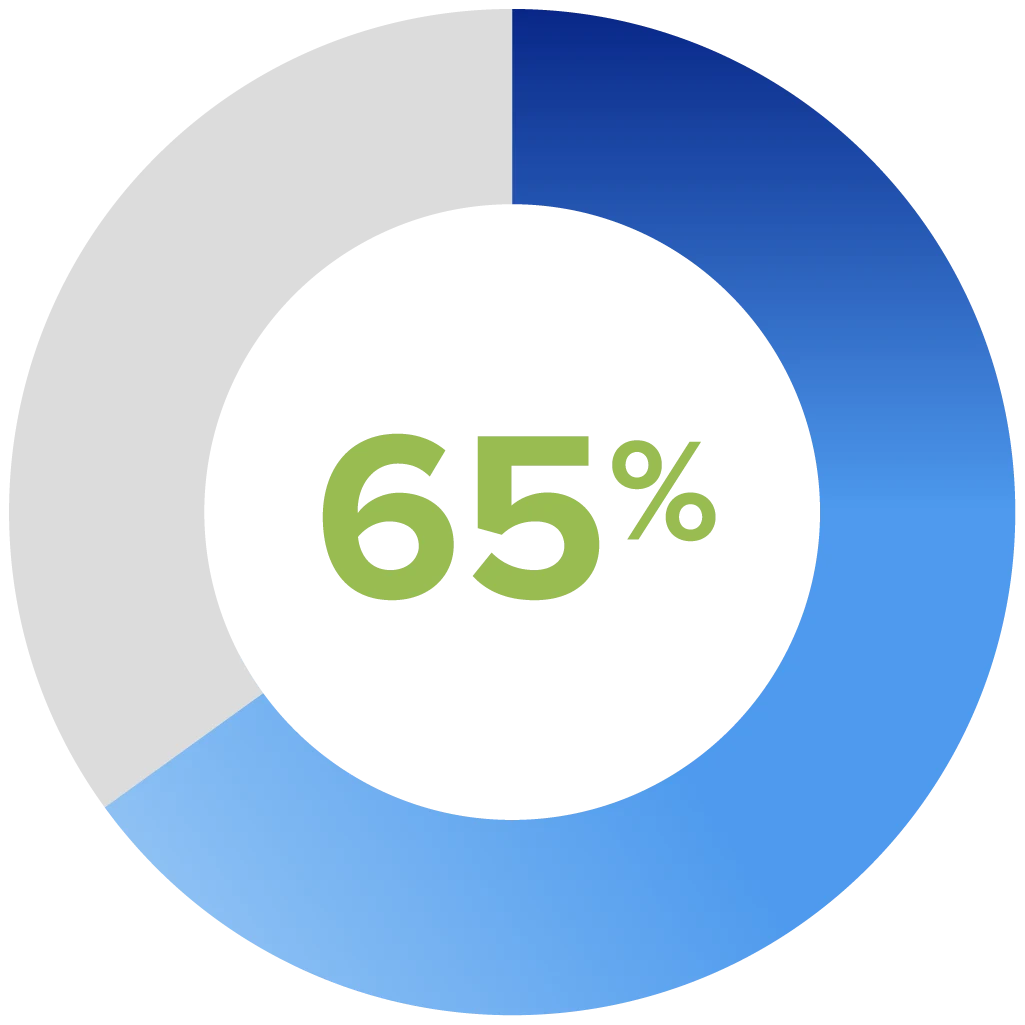

65% of global leaders cite “talent and leadership shortages” as their #1 business challenge.

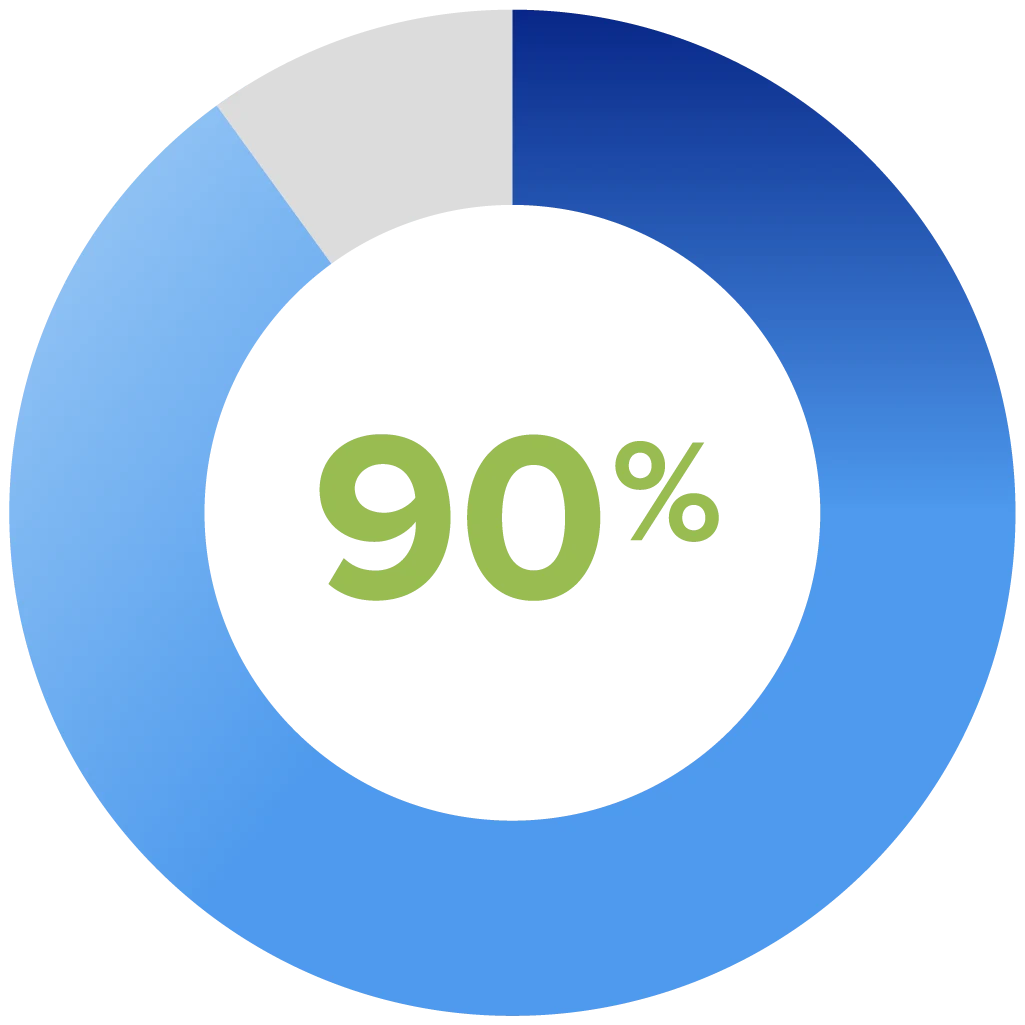

A full 90% of organizations do not have all the skills they need to be successful.

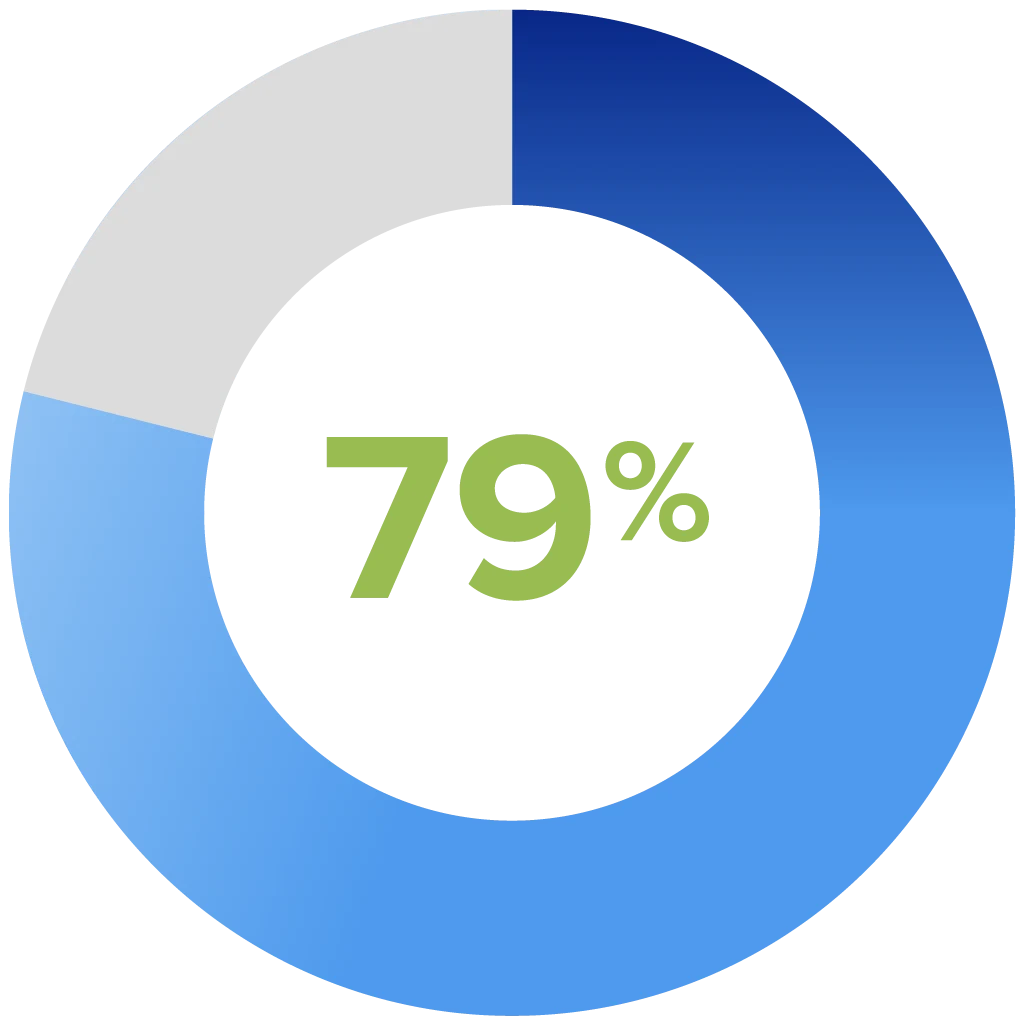

79% of L&D pros agree: it’s less expensive to reskill a current employee than to hire a new one.