Which of the following statements is a basic element of the auditor's standard report on a nonissuer's financial statements?

Below is the code for an example image modal link

Flashcards

/* -- Un-comment the code below to show all parts of question -- */

| A. The disclosures provide reasonable assurance that the financial statements are free of material misstatement. | ||

| B. The auditor evaluated the overall internal control. | ||

| C. An audit includes assessing significant estimates made by management. | ||

| D. The financial statements are consistent with those of the prior period. |

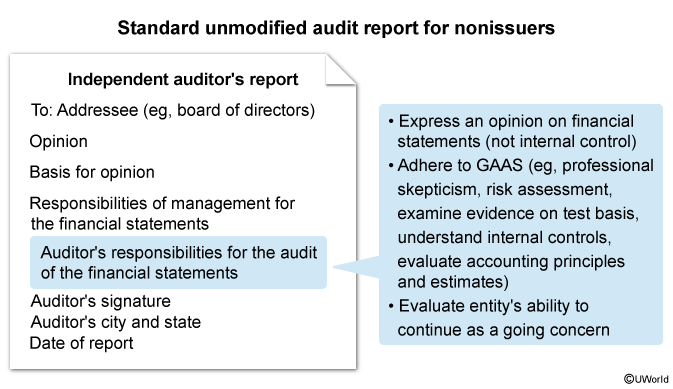

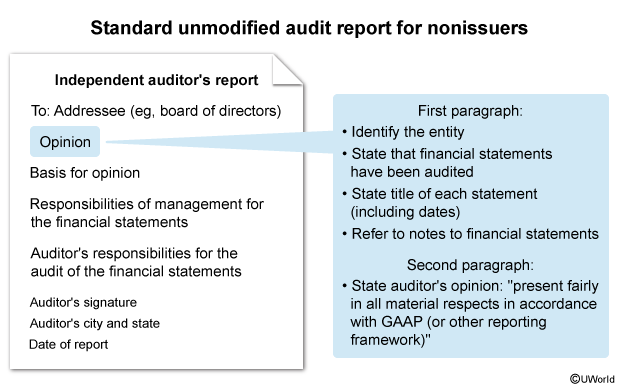

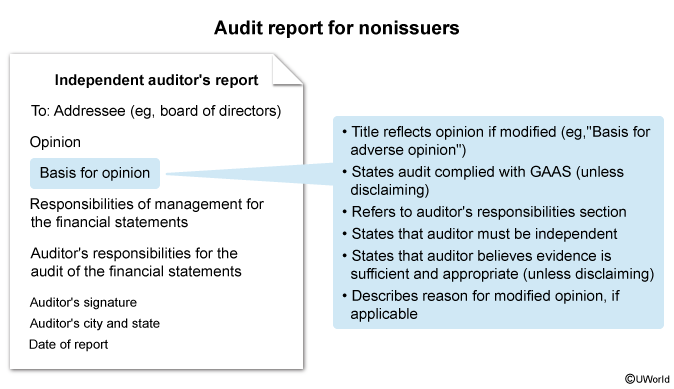

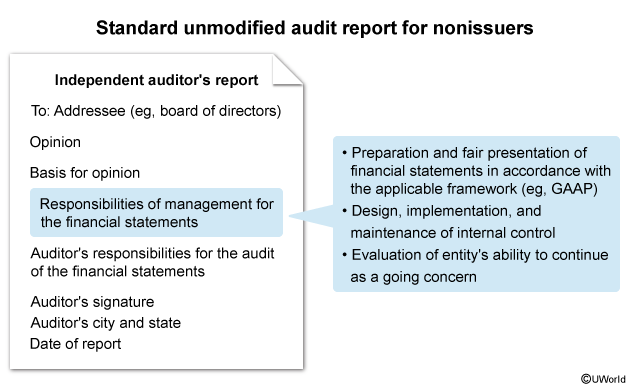

GAAS outlines the structure of a standard audit report for nonissuers. The order and content are regimented to make them easier to understand and compare. The standard report consists of the opinion, basis for opinion, auditor's responsibilities, and management's responsibilities sections.

The section titled "Auditor's Responsibilities for the Audit of the F/S" includes a general description of an audit. It indicates that the auditor evaluated the appropriateness of management's accounting policies, the reasonableness of its significant accounting estimates, and the overall presentation of the F/S. It also includes references to tests performed in all F/S audits, including risk assessment, understanding (not evaluating) I/C, and the examination of evidence on a test basis (Choice B).

(Choice A) Because disclosures are an element of the F/S, they cannot provide assurance that those F/S are free of material misstatement. The auditor provides that assurance on the basis of audit evidence.

(Choice D) The opinion section of the standard nonissuer's audit report states that the F/S are presented in accordance with GAAP, but it does not mention consistency explicitly.

Things to remember:

The auditor's responsibilities section of a standard audit report for a nonissuer's F/S includes a general description of an audit, including the assessment of estimates and accounting policies used by management.

Lecture References :

- AUD 19.01 : Specific matters that require special consideration : Accounting estimates

{kind=link}

{kind=link}

{kind=link}

{kind=link}