Which of the following objectives is achieved when an auditor decides to employ classical variable sampling?

Below is the code for an example image modal link

Flashcards

/* -- Un-comment the code below to show all parts of question -- */

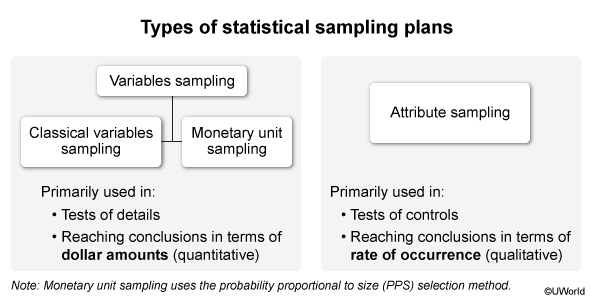

Methods of statistical sampling can be categorized as variable sampling or attribute sampling. Variable sampling (including classical and probability proportional to size) is commonly used in tests of details. It involves estimating a quantity or dollar amount of a population. Attribute sampling is generally used in control testing. It involves estimating the rate of occurrence of a quality or characteristic (eg, improperly processed vouchers A document prepared by the accounts payable clerk to request that a check be issued to a vendor in payment for goods or services received., unrecorded billings) in a population (Choices A and B).

Because most companies carry much more inventory than can be examined in an audit, auditors often rely on sampling to test inventory. After selecting a random sample of inventory from a company's records, an auditor can determine whether each item in the sample is actually held in inventory and is in saleable condition. Extrapolating from the sample allows the auditor to estimate the quantity of the entire population. This is an example of classical variable sampling.

(Choice D) F/S auditors may assess the effectiveness (not efficiency) of a payroll system by using attribute (not variable) sampling to determine the rate of deviation for various controls within the system.

Things to remember:

Variable sampling is commonly used in tests of details and involves estimating the quantity or dollar amount of a population. Attribute sampling is generally used in control testing and involves estimating the rate of occurrence of a quality or characteristic in a population.

Lecture References :

- AUD 7.03 : Audit Sampling : Variables Sampling

{kind=link}